Navigating the "Golden Triangle" of Healthcare: Why Your Effort is the Best Insurance

At their core, insurance companies are for-profit entities. Like any business with a fiduciary responsibility to shareholders, their primary objective is to maximize revenue (or premiums collected) while minimizing expenditures (or claims paid out). In the world of healthcare, this often creates a fundamental disconnect: the insurer’s goal is profit, while the subscriber’s goal is wellness.

When an insurance carrier limits coverage, the financial burden shifts directly to the patient. While you cannot control market prices or corporate coverage ceilings, you do hold a significant "hidden" power: the ability to lower your long-term costs through a personal investment in your own well-being.

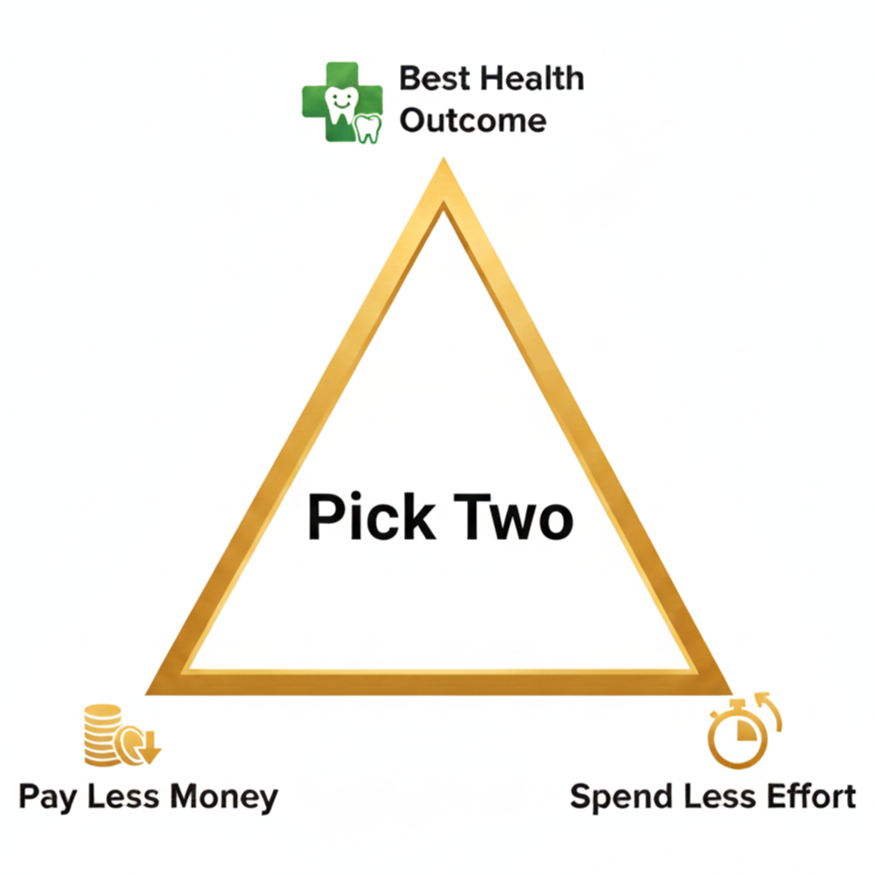

The Golden Triangle of Healthcare

To understand how to navigate this system, we can apply the "Golden Triangle" rule. In this model, there are three competing factors:

Quality of Outcome (The best healthcare results)

Financial Investment (Money spent)

Personal Effort (Preventative care and lifestyle)

The rule of the triangle is simple: You can pick two, but you cannot have all three.

Low Money + Low Effort = Poor Outcomes: This is the "emergency-only" route. You save time and immediate cash, but your health inevitably declines.

Low Money + Best Outcome = High Effort: You achieve great health without breaking the bank, but it requires rigorous personal discipline.

Low Effort + Best Outcome = High Money: You can maintain your health while remaining passive, but you will pay a premium for providers to "fix" what you aren't maintaining.

To see this triangle in action, consider three different patients:

The High-Effort Success:

John chooses Best Outcome and Low Money. He maintains a low-sugar diet and a meticulous hygiene routine. Because he invests heavily in Personal Effort, he avoids catastrophic, expensive procedures. For John, insurance is truly just a safety net; his lifelong discipline keeps his actual healthcare costs at a minimum.

The Outsourced Effort:

Jane chooses Best Outcome and Low Effort. She enjoys sweets and has mild gum disease, but she expects the highest standard of care. She relies on her provider to use cutting-edge technology and premium materials to "save" her smile. Because Jane has outsourced the effort to her doctor, she must pay significantly more out-of-pocket to achieve her desired results.

The Insurance Trap:

Paul operates on Low Money and Low Effort. He only visits the dentist during emergencies and suffers from systemic health issues. Because he invests neither time nor money into prevention, he is forced to accept whatever treatment his insurance deems "acceptable"—usually the Least Expensive Alternative Treatment (LEAT). Rather than saving a tooth, Paul ends up with an extraction. Low effort and low investment consistently lead to the poorest health outcomes.

The Reality of the "Coupon Book"

Insurance companies view your policy like a coupon book. They maximize their profit on "Johns" because they collect premiums while paying out almost nothing in claims. Conversely, they must strictly control the "coverage ceiling" for people like Jane and Paul.

Unfortunately for Paul, the "coupons" in his book don't compound. If he doesn't use his benefits for preventative care one year, he doesn't get double the coverage the next. By only paying for the cheapest possible fix, insurance effectively dictates a patient's treatment plan.

Taking Back Control

The takeaway is clear: if you want the Best Health Outcome without spending a fortune (Low Money), the only variable you can control is your Effort.

Insurance companies will always prioritize the LEAT. To break free from that cycle, you must be willing to invest in yourself. By shifting your focus from "What does my insurance cover?" to "How much effort can I invest?", you take the power away from the shareholders and put it back where it belongs: in your own hands.